Prerequisites: ch058 (Linear), ch059 (Quadratic), ch042 (Exponential Growth)

Concepts: Compound interest, exponential vs logistic growth, present value, IRR

Output: Multi-scenario investment comparison with NPV, IRR, and sensitivity

Difficulty: Intermediate | ~45 minutes

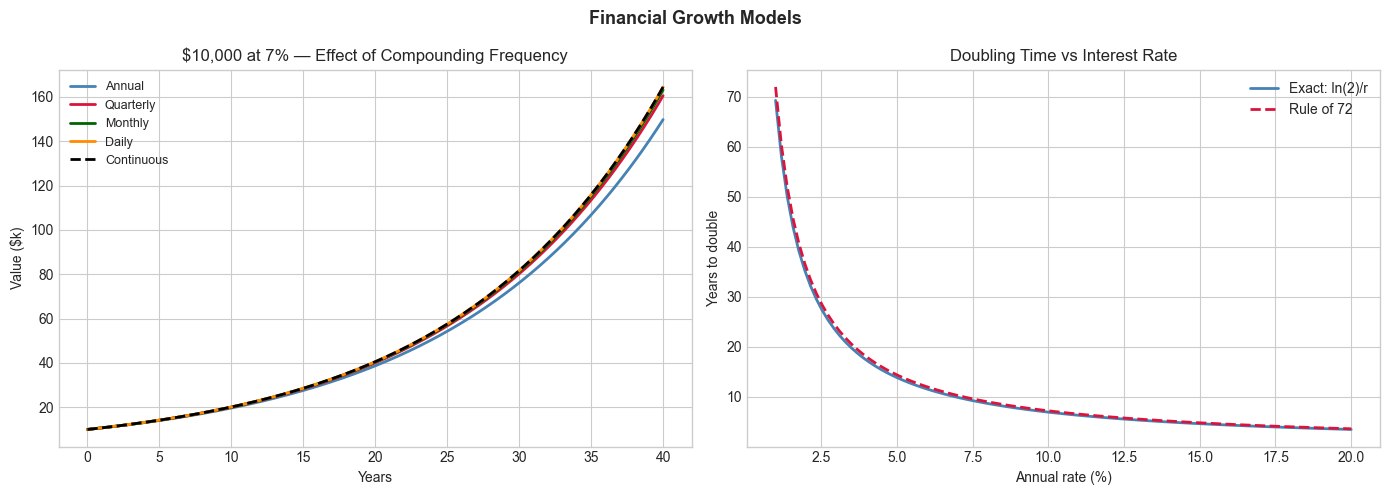

Stage 1 — Setup and Compound Interest¶

import numpy as np

import matplotlib.pyplot as plt

plt.style.use('seaborn-v0_8-whitegrid')

def compound_interest(P, r, n, t):

"""Compound interest: A = P(1 + r/n)^(nt)."""

return P * (1 + r/n)**(n*t)

def continuous_compound(P, r, t):

"""Continuous compounding: A = P*e^(rt)."""

return P * np.exp(r * t)

P0, r = 10000, 0.07 # $10k at 7% annual

t = np.linspace(0, 40, 400)

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

for n, label, color in [(1,'Annual','steelblue'),(4,'Quarterly','crimson'),(12,'Monthly','darkgreen'),(365,'Daily','darkorange')]:

axes[0].plot(t, compound_interest(P0, r, n, t)/1000, color=color, linewidth=2, label=label)

axes[0].plot(t, continuous_compound(P0, r, t)/1000, 'k--', linewidth=2, label='Continuous')

axes[0].set_title('$10,000 at 7% — Effect of Compounding Frequency')

axes[0].set_xlabel('Years'); axes[0].set_ylabel('Value ($k)'); axes[0].legend(fontsize=9)

# Doubling time: rule of 72 (approx) vs exact

rates = np.linspace(0.01, 0.20, 100)

exact_double = np.log(2) / rates

rule72 = 72 / (rates * 100)

axes[1].plot(rates*100, exact_double, color='steelblue', linewidth=2, label='Exact: ln(2)/r')

axes[1].plot(rates*100, rule72, color='crimson', linewidth=2, linestyle='--', label='Rule of 72')

axes[1].set_title('Doubling Time vs Interest Rate'); axes[1].set_xlabel('Annual rate (%)')

axes[1].set_ylabel('Years to double'); axes[1].legend()

plt.suptitle('Financial Growth Models', fontsize=13, fontweight='bold')

plt.tight_layout(); plt.show()

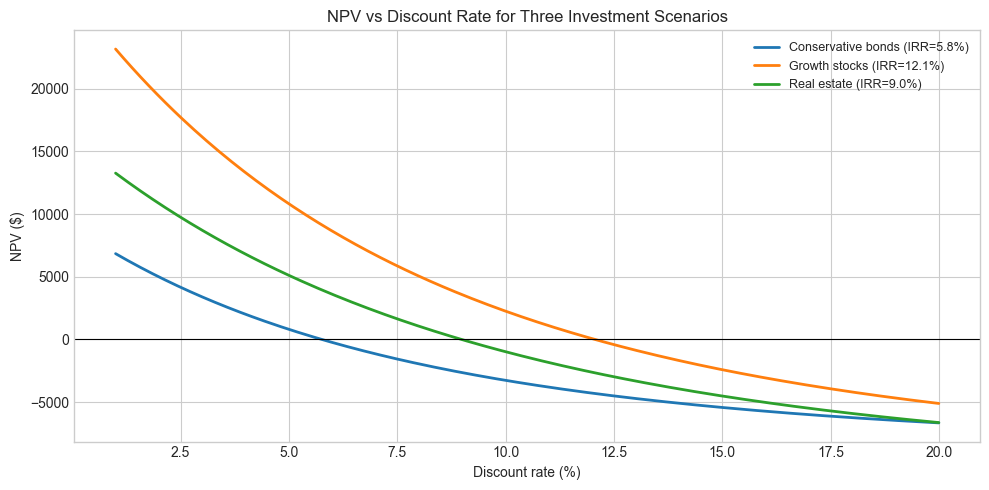

Stage 2 — NPV and IRR¶

# Net Present Value and Internal Rate of Return

def npv(cashflows, rate):

"""NPV: Σ CFₜ / (1+r)^t."""

return sum(cf / (1+rate)**t for t, cf in enumerate(cashflows))

def irr(cashflows, tol=1e-6, max_iter=100):

"""Find IRR: the rate where NPV=0 (bisection method)."""

lo, hi = -0.999, 10.0

for _ in range(max_iter):

mid = (lo + hi) / 2

if npv(cashflows, mid) > 0:

lo = mid

else:

hi = mid

if hi - lo < tol:

break

return mid

# Compare three investment scenarios

scenarios = {

'Conservative bonds': [-10000] + [600]*15 + [10000],

'Growth stocks': [-10000] + [-500]*3 + [2000]*12 + [15000],

'Real estate': [-10000, -2000] + [800]*10 + [20000],

}

rates = np.linspace(0.01, 0.20, 200)

fig, ax = plt.subplots(figsize=(10, 5))

for name, cfs in scenarios.items():

npvs = [npv(cfs, r) for r in rates]

irr_val = irr(cfs)

ax.plot(rates*100, npvs, linewidth=2, label=f'{name} (IRR={irr_val*100:.1f}%)')

ax.axhline(0, color='black', linewidth=0.8)

ax.set_title('NPV vs Discount Rate for Three Investment Scenarios')

ax.set_xlabel('Discount rate (%)'); ax.set_ylabel('NPV ($)'); ax.legend(fontsize=9)

plt.tight_layout(); plt.show()

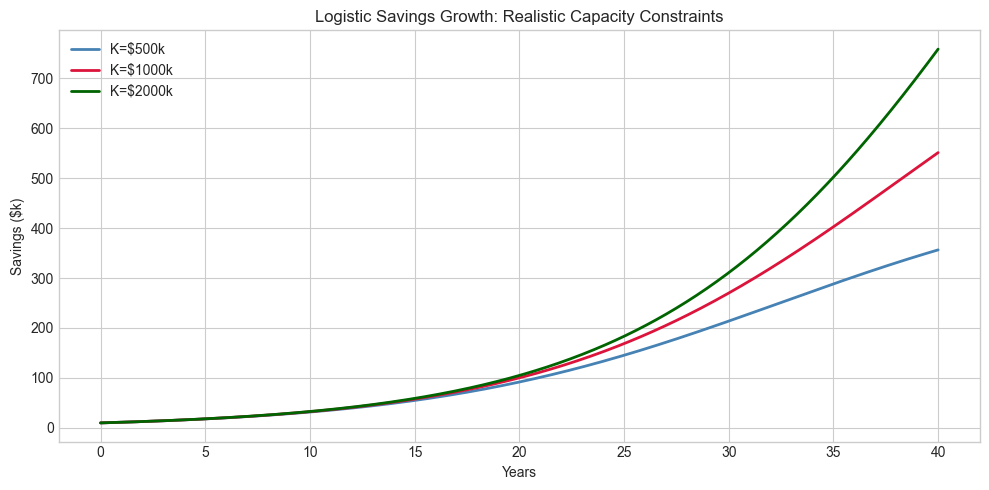

Stage 3 — Logistic Savings Model¶

# Savings with diminishing returns (logistic model)

# Motivated by: hard to save the first $100k, harder still above that

def savings_model(t, S0, K, r):

"""Logistic savings growth with capacity K."""

return K / (1 + (K/S0 - 1) * np.exp(-r * t))

t = np.linspace(0, 40, 500)

fig, ax = plt.subplots(figsize=(10, 5))

for K, color in [(500000,'steelblue'),(1000000,'crimson'),(2000000,'darkgreen')]:

ax.plot(t, savings_model(t, 10000, K, 0.12)/1000, color=color, linewidth=2, label=f'K=${K//1000}k')

ax.set_title('Logistic Savings Growth: Realistic Capacity Constraints')

ax.set_xlabel('Years'); ax.set_ylabel('Savings ($k)'); ax.legend()

plt.tight_layout(); plt.show()

Results & Reflection¶

What was built: Compound interest calculator, NPV/IRR analysis, and logistic savings model.

Math used: Exponential growth (ch042), logistic functions (ch064), iterative root finding for IRR (ch074).

Extensions: 1) Add inflation-adjusted returns. 2) Monte Carlo simulation with random return rates. 3) Compare DCA vs lump-sum investing strategies.