Prerequisites: ch070 (Function Families), ch017 (Mathematical Modeling)

You will learn:

Apply the modeling cycle: observe → hypothesize → fit → validate

Choose an appropriate function family for a real dataset

Understand the difference between interpolation and extrapolation

Recognize when a model is wrong

Environment: Python 3.x, numpy, matplotlib

1. Concept¶

Mathematical modeling is the process of representing a real-world phenomenon with a mathematical function.

The modeling cycle:

Observe: collect data or describe the phenomenon qualitatively

Hypothesize: propose a function family (linear? exponential? logistic?)

Fit: find parameter values that minimize error on observed data

Validate: test on held-out data; check assumptions

Refine or reject: revise hypothesis if validation fails

Interpolation vs extrapolation:

Interpolation: predicting within the range of observed data — generally reliable

Extrapolation: predicting beyond the data range — dangerous; model structure must be trusted

When a model is wrong:

Residuals show systematic patterns (not random) → wrong function family

Model fits training data but fails on new data → overfitting

Model misses obvious features → underfitting or wrong family

(Recall ch017: mathematical models are simplifications. All models are wrong; some are useful.)

2. Intuition & Mental Models¶

Physical analogy: A weather forecast is a model. The model’s function family (atmospheric equations) encodes physical laws. Parameter fitting uses observed pressure, temperature, humidity. Validation happens the next day. If the forecast is systematically wrong in a direction, the model structure needs revision.

Computational analogy: Machine learning is automated modeling. The algorithm searches over a hypothesis class (function family) and finds parameters that minimize error. The same cycle applies: train, validate, revise architecture.

3. Visualization¶

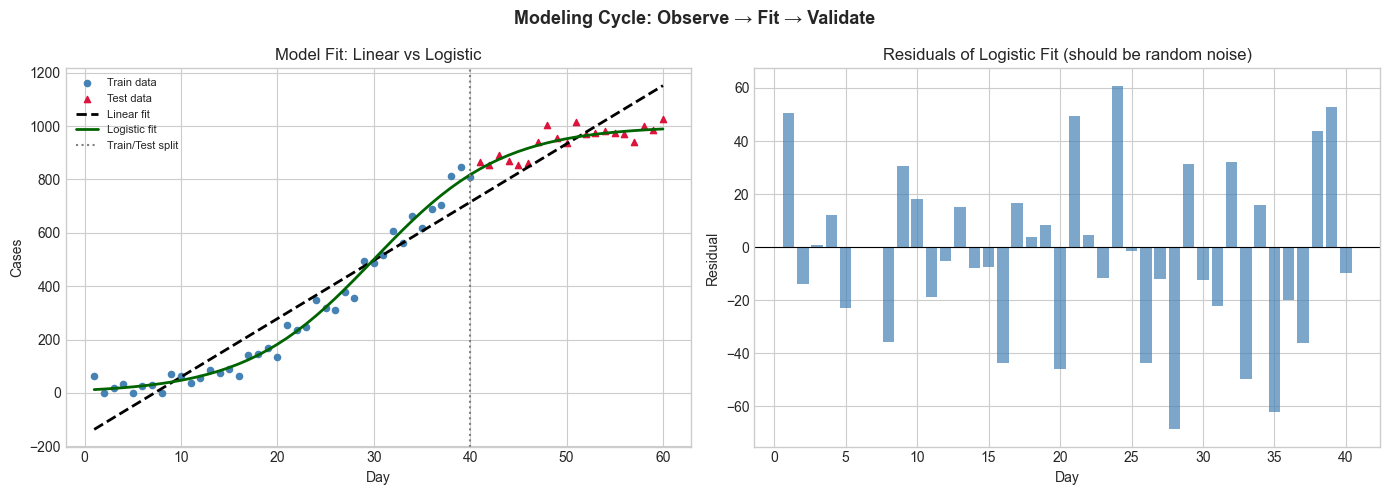

# --- Visualization: The full modeling cycle on real-shaped data ---

import numpy as np

import matplotlib.pyplot as plt

plt.style.use('seaborn-v0_8-whitegrid')

np.random.seed(7)

# Generate data from a logistic process (unknown to the modeler)

t = np.arange(1, 61)

K, r, t0 = 1000, 0.15, 30

true_y = K / (1 + np.exp(-r * (t - t0)))

observed = true_y + np.random.normal(0, 30, len(t))

observed = np.maximum(0, observed)

# Modeler's hypothesis 1: linear

t_train, t_test = t[:40], t[40:]

y_train, y_test = observed[:40], observed[40:]

# Fit linear model to training data

A = np.column_stack([t_train, np.ones(len(t_train))])

m_lin, b_lin = np.linalg.lstsq(A, y_train, rcond=None)[0]

y_pred_lin = m_lin * t + b_lin

# Fit logistic by simple grid search (preview of ch072)

best_err, best_params = np.inf, None

for K_try in [800, 1000, 1200]:

for r_try in [0.1, 0.15, 0.2]:

for t0_try in [25, 30, 35]:

y_hat = K_try / (1 + np.exp(-r_try * (t_train - t0_try)))

err = np.mean((y_hat - y_train)**2)

if err < best_err:

best_err, best_params = err, (K_try, r_try, t0_try)

Kb, rb, t0b = best_params

y_pred_log = Kb / (1 + np.exp(-rb * (t - t0b)))

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

ax = axes[0]

ax.scatter(t_train, y_train, color='steelblue', s=20, label='Train data')

ax.scatter(t_test, y_test, color='crimson', s=20, label='Test data', marker='^')

ax.plot(t, y_pred_lin, 'k--', linewidth=2, label=f'Linear fit')

ax.plot(t, y_pred_log, color='darkgreen', linewidth=2, label=f'Logistic fit')

ax.axvline(40, color='gray', linestyle=':', linewidth=1.5, label='Train/Test split')

ax.set_title('Model Fit: Linear vs Logistic'); ax.set_xlabel('Day'); ax.set_ylabel('Cases')

ax.legend(fontsize=8)

# Residuals for logistic model

residuals = y_train - Kb/(1+np.exp(-rb*(t_train - t0b)))

axes[1].bar(t_train, residuals, color='steelblue', alpha=0.7)

axes[1].axhline(0, color='black', linewidth=0.8)

axes[1].set_title('Residuals of Logistic Fit (should be random noise)')

axes[1].set_xlabel('Day'); axes[1].set_ylabel('Residual')

plt.suptitle('Modeling Cycle: Observe → Fit → Validate', fontsize=13, fontweight='bold')

plt.tight_layout()

plt.show()

lin_test_err = np.sqrt(np.mean((y_pred_lin[40:] - y_test)**2))

log_test_err = np.sqrt(np.mean((y_pred_log[40:] - y_test)**2))

print(f"Linear model test RMSE: {lin_test_err:.1f}")

print(f"Logistic model test RMSE: {log_test_err:.1f}")

Linear model test RMSE: 87.4

Logistic model test RMSE: 30.7

5. Python Implementation¶

# --- Implementation: Modeling pipeline ---

import numpy as np

class SimpleFitter:

"""Fit and evaluate a parameterized model using grid search."""

def __init__(self, model_fn, param_grid):

self.model_fn = model_fn

self.param_grid = param_grid

self.best_params = None

self.best_mse = np.inf

def fit(self, x, y):

"""Grid search over param_grid to minimize MSE."""

import itertools

keys = list(self.param_grid.keys())

values = [self.param_grid[k] for k in keys]

for combo in itertools.product(*values):

params = dict(zip(keys, combo))

try:

y_hat = self.model_fn(x, **params)

mse = np.mean((y - y_hat)**2)

if mse < self.best_mse:

self.best_mse, self.best_params = mse, params

except (ValueError, RuntimeWarning, FloatingPointError):

continue

return self

def predict(self, x):

return self.model_fn(x, **self.best_params)

def score(self, x, y):

y_hat = self.predict(x)

ss_res = np.sum((y - y_hat)**2)

ss_tot = np.sum((y - y.mean())**2)

return 1 - ss_res / ss_tot # R²

# Use on growth data

np.random.seed(0)

t = np.linspace(1, 50, 50)

y_true = 500 / (1 + np.exp(-0.2*(t - 25)))

y_obs = y_true + np.random.normal(0, 15, 50)

fitter = SimpleFitter(

model_fn=lambda t, K, r, t0: K / (1 + np.exp(-r*(t - t0))),

param_grid={'K': [400, 500, 600], 'r': [0.15, 0.2, 0.25], 't0': [20, 25, 30]}

)

fitter.fit(t, y_obs)

print("Best params:", fitter.best_params)

print("R² score:", fitter.score(t, y_obs).round(4))Best params: {'K': 500, 'r': 0.2, 't0': 25}

R² score: 0.9919

6. Experiments¶

Experiment 1: Use the SimpleFitter on linear data with a logistic model. What happens? The logistic will try to fit a plateau where there is none — high residuals at the extremes.

Experiment 2: Vary the noise level (σ) from 5 to 100 and observe how the best fit degrades. At what noise level does model selection become unreliable?

7. Exercises¶

Easy 1. A population grows from 100 to 800 over 20 years. Which function family is most appropriate: linear, exponential, or logistic? Justify with one qualitative reason.

Easy 2. If residuals in a model show a clear wave pattern, what does this suggest about the model’s function family?

Medium 1. Implement a train-test split evaluator: given data, a model fn, and a split ratio, fit on train and compute RMSE on test. Apply to at least two model families on the same dataset.

Medium 2. Generate data from y = 3x² + noise. Fit linear, quadratic, and cubic models. Which has lowest training error? Which has lowest test error?

Hard. Implement AIC (Akaike Information Criterion) model comparison: AIC = 2k - 2·log(L), where k is the number of parameters and L is the likelihood (assume Gaussian errors). Compare linear, quadratic, and cubic fits using AIC.

9. Chapter Summary & Connections¶

Modeling cycle: observe → hypothesize family → fit → validate → refine

Interpolation is reliable; extrapolation requires trust in the model structure

Residuals should look like random noise — any pattern indicates model misspecification

RMSE, R², AIC are quantitative tools for comparing models

Forward connections:

ch072 (Fitting Simple Models) formalizes the parameter search

ch073 (Error and Residuals) analyzes what residual patterns tell us

ch287 (Model Evaluation) covers the full validation toolkit