Part VIII: Probability | Computational Mathematics for Programmers

1. Rare Events in Large Trials¶

The Poisson distribution models counts of rare events in a fixed interval of time, space, or any other dimension.

Conditions for a Poisson process:

Events occur independently

The average rate λ is constant

Two events cannot occur at the exact same instant

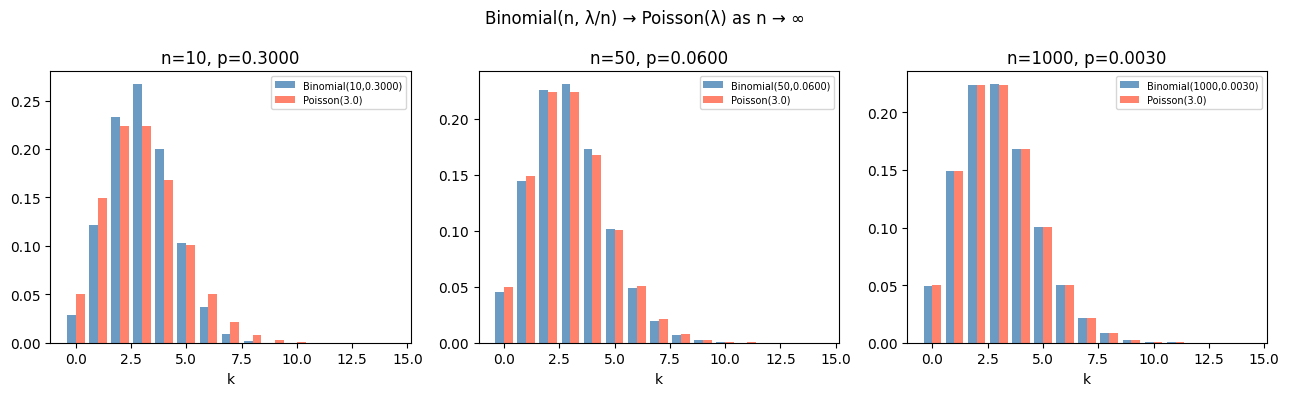

It arises as the limit of Binomial(n, p) as n→∞, p→0, with np = λ fixed.

2. Derivation from Binomial¶

Take X ~ Binomial(n, λ/n). As n→∞:

(The exponential e^{-λ} = lim(1-λ/n)^n uses the exponential function from ch041.)

The Poisson PMF:

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

from math import factorial, exp

def poisson_pmf(lam, k):

"""P(X=k) for X ~ Poisson(lambda). From scratch."""

return (lam**k * exp(-lam)) / factorial(k)

# Verify against scipy

lam = 3.0

print("Poisson(λ=3) PMF:")

for k in range(12):

ours = poisson_pmf(lam, k)

ref = stats.poisson.pmf(k, lam)

bar = '█' * int(ours * 60)

print(f" k={k:2d}: {ours:.5f} {bar}")Poisson(λ=3) PMF:

k= 0: 0.04979 ██

k= 1: 0.14936 ████████

k= 2: 0.22404 █████████████

k= 3: 0.22404 █████████████

k= 4: 0.16803 ██████████

k= 5: 0.10082 ██████

k= 6: 0.05041 ███

k= 7: 0.02160 █

k= 8: 0.00810

k= 9: 0.00270

k=10: 0.00081

k=11: 0.00022

3. Mean and Variance¶

For X ~ Poisson(λ):

The mean equals the variance — this is unique to the Poisson distribution and is a quick check: if a count variable has mean ≈ variance, Poisson is a reasonable model.

# Simulate Poisson processes and verify E[X] = Var(X) = lambda

rng = np.random.default_rng(seed=42)

n = 100_000

print(f"{'λ':>6} {'Sample Mean':>14} {'Sample Var':>12} {'Mean≈λ':>8} {'Var≈λ':>8}")

print("-" * 55)

for lam in [0.5, 1.0, 3.0, 10.0, 30.0]:

samples = rng.poisson(lam, size=n)

m = samples.mean()

v = samples.var()

print(f"{lam:>6.1f} {m:>14.4f} {v:>12.4f} {abs(m-lam)<0.05!s:>8} {abs(v-lam)<0.05!s:>8}") λ Sample Mean Sample Var Mean≈λ Var≈λ

-------------------------------------------------------

0.5 0.5008 0.5004 True True

1.0 1.0014 1.0038 True True

3.0 2.9971 2.9844 True True

10.0 10.0160 10.0099 True True

30.0 29.9750 29.7557 True False

# Binomial -> Poisson convergence

lam = 3.0

k_range = np.arange(0, 15)

fig, axes = plt.subplots(1, 3, figsize=(13, 4))

for ax, n in zip(axes, [10, 50, 1000]):

p = lam / n

binom_pmf = stats.binom.pmf(k_range, n, p)

pois_pmf = stats.poisson.pmf(k_range, lam)

ax.bar(k_range - 0.2, binom_pmf, width=0.4, alpha=0.8, color='steelblue', label=f'Binomial({n},{p:.4f})')

ax.bar(k_range + 0.2, pois_pmf, width=0.4, alpha=0.8, color='tomato', label=f'Poisson({lam})')

ax.set_title(f'n={n}, p={p:.4f}')

ax.set_xlabel('k')

ax.legend(fontsize=7)

plt.suptitle('Binomial(n, λ/n) → Poisson(λ) as n → ∞', fontsize=12)

plt.tight_layout()

plt.show()

4. Poisson Process Applications¶

# Application 1: Server requests

# A web server receives 120 requests/minute on average.

# What is P(>130 requests in a given minute)?

lam_server = 120 # average requests per minute

threshold = 130

rv = stats.poisson(lam_server)

p_exceed = 1 - rv.cdf(threshold)

print(f"Server load: λ={lam_server} requests/min")

print(f"P(X > {threshold}) = {p_exceed:.6f} ({p_exceed*100:.3f}%)")

# Application 2: Inter-arrival times follow Exponential distribution

# If events arrive at rate λ, the time between events is Exponential(λ)

# P(wait > t) = exp(-λt)

lam_arrivals = 2.0 # 2 events per minute

t_wait = 1.0 # wait time in minutes

p_wait_over_t = np.exp(-lam_arrivals * t_wait)

print(f"\nInter-arrival: λ={lam_arrivals}/min")

print(f"P(wait > {t_wait} min) = exp(-{lam_arrivals}×{t_wait}) = {p_wait_over_t:.4f}")

# Simulate inter-arrival times

rng = np.random.default_rng(seed=0)

n_sim = 100_000

inter_arrivals = rng.exponential(scale=1/lam_arrivals, size=n_sim)

print(f"Simulated P(wait > {t_wait}) = {(inter_arrivals > t_wait).mean():.4f}")Server load: λ=120 requests/min

P(X > 130) = 0.168518 (16.852%)

Inter-arrival: λ=2.0/min

P(wait > 1.0 min) = exp(-2.0×1.0) = 0.1353

Simulated P(wait > 1.0) = 0.1353

5. Poisson Regression Preview¶

When modeling count data (number of defects, number of accidents, number of page views), the Poisson distribution provides the likelihood function. Poisson regression models log(λ) as a linear function of features — this is a generalized linear model used throughout data science.

# Overdispersion check: real count data often has Var > Mean (overdispersed)

# This violates the Poisson assumption and signals a different model is needed

# Underdispersed (Poisson): traffic accidents at a junction

lam = 2.0

n_days = 1000

rng = np.random.default_rng(seed=42)

poisson_data = rng.poisson(lam, size=n_days)

print("Poisson data (accidents per day):")

print(f" Mean = {poisson_data.mean():.4f} (expected: {lam})")

print(f" Var = {poisson_data.var():.4f} (expected: {lam})")

print(f" Var/Mean = {poisson_data.var()/poisson_data.mean():.4f} (Poisson: should ≈ 1)")Poisson data (accidents per day):

Mean = 2.0090 (expected: 2.0)

Var = 2.0049 (expected: 2.0)

Var/Mean = 0.9980 (Poisson: should ≈ 1)

6. Summary¶

Poisson(λ) models the count of rare independent events in a fixed interval.

PMF: P(X=k) = λ^k · e^{−λ} / k!.

E[X] = Var(X) = λ — the Poisson’s defining property.

It is the limit of Binomial(n, λ/n) as n→∞.

Inter-arrival times in a Poisson process are Exponential(λ).

7. Forward References¶

The Poisson distribution is the foundation of Poisson regression (a generalized linear model) covered in Part IX statistics. It connects to the exponential distribution, which appears in survival analysis and queuing theory. The normal approximation to the Poisson (valid for large λ) is another instance of the Central Limit Theorem (ch254).