Part VII — Calculus¶

Unconstrained optimisation finds the minimum of f(x) over all x. Most real problems are constrained: minimise cost subject to a budget, maximise accuracy subject to a memory limit. This chapter develops the mathematical machinery — Lagrange multipliers and KKT conditions — and connects it to ML regularisation and support vector machines.

(Builds on ch212 — Gradient Descent, ch214 — Saddle Points)

1. The Equality-Constrained Problem¶

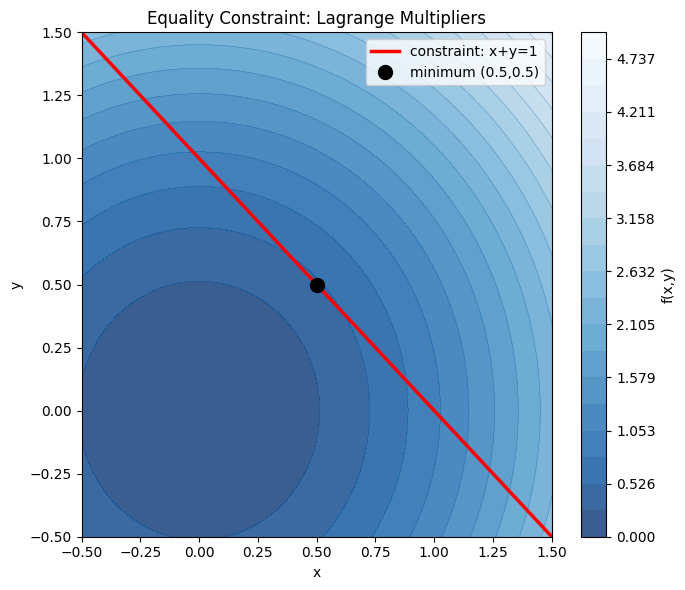

Problem: minimise f(x,y) subject to g(x,y) = 0.

Key insight: at the constrained minimum, the gradient of f must be parallel to the gradient of g — otherwise you could move along the constraint surface and decrease f.

This gives the Lagrangian: L(x, y, λ) = f(x,y) − λ·g(x,y)

Setting ∇L = 0 yields: ∇f = λ∇g and g(x,y) = 0

import numpy as np

import matplotlib.pyplot as plt

from matplotlib import cm

# Minimise f(x,y) = x^2 + y^2 subject to x + y = 1

# Lagrangian: L = x^2 + y^2 - lam*(x + y - 1)

# dL/dx = 2x - lam = 0 => x = lam/2

# dL/dy = 2y - lam = 0 => y = lam/2

# constraint: x + y = 1 => lam = 1 => x = y = 0.5

x_opt, y_opt = 0.5, 0.5

f_opt = x_opt**2 + y_opt**2

print(f'Analytical solution: x={x_opt}, y={y_opt}, f={f_opt}')

# Visualise

x = np.linspace(-1, 2, 300)

y = np.linspace(-1, 2, 300)

X, Y = np.meshgrid(x, y)

F = X**2 + Y**2

fig, ax = plt.subplots(figsize=(7, 6))

levels = np.linspace(0, 5, 20)

cs = ax.contourf(X, Y, F, levels=levels, cmap='Blues_r', alpha=0.8)

ax.contour(X, Y, F, levels=levels, colors='steelblue', linewidths=0.5, alpha=0.5)

plt.colorbar(cs, ax=ax, label='f(x,y)')

# Constraint line x + y = 1

x_line = np.linspace(-0.5, 1.5, 200)

y_line = 1 - x_line

ax.plot(x_line, y_line, 'r-', lw=2.5, label='constraint: x+y=1')

ax.plot(x_opt, y_opt, 'ko', ms=10, zorder=5, label=f'minimum ({x_opt},{y_opt})')

ax.set_xlabel('x'); ax.set_ylabel('y')

ax.set_title('Equality Constraint: Lagrange Multipliers')

ax.legend(); ax.set_xlim(-0.5, 1.5); ax.set_ylim(-0.5, 1.5)

plt.tight_layout()

plt.savefig('ch233_equality.png', dpi=120)

plt.show()

print('The minimum on the constraint line is where the circular level curve is tangent to the line.')Analytical solution: x=0.5, y=0.5, f=0.5

The minimum on the constraint line is where the circular level curve is tangent to the line.

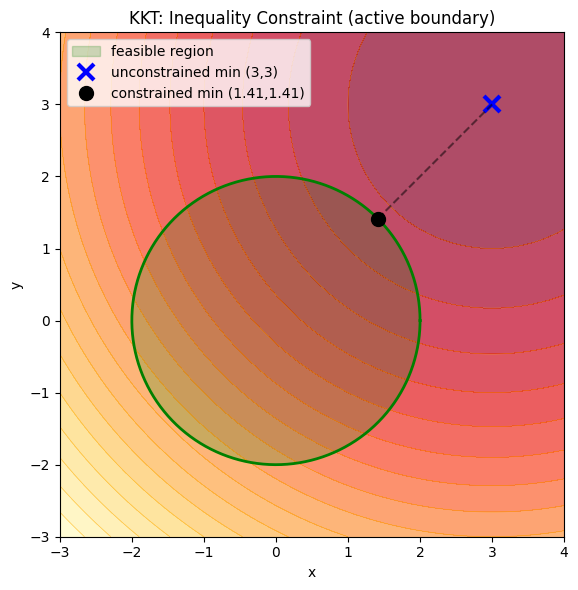

2. KKT Conditions for Inequality Constraints¶

Problem: minimise f(x) subject to g(x) ≤ 0.

The Karush-Kuhn-Tucker (KKT) conditions extend Lagrange multipliers:

Stationarity: ∇f + μ∇g = 0

Primal feasibility: g(x) ≤ 0

Dual feasibility: μ ≥ 0

Complementary slackness: μ·g(x) = 0

Condition 4 means either the constraint is active (g=0) or the multiplier is zero. This is the mathematical foundation of support vectors in SVMs — most training points have μ=0; only the points on the margin boundary matter.

# KKT example: minimise (x-3)^2 + (y-3)^2 subject to x^2 + y^2 <= 4

# Unconstrained minimum is (3,3) — outside the feasible region (circle r=2)

# So the constrained minimum is on the boundary: x^2 + y^2 = 4

# Lagrangian: L = (x-3)^2 + (y-3)^2 + mu*(x^2 + y^2 - 4)

# Stationarity:

# 2(x-3) + 2*mu*x = 0 => x(1+mu) = 3

# 2(y-3) + 2*mu*y = 0 => y(1+mu) = 3

# So x = y = 3/(1+mu)

# Constraint active: x^2 + y^2 = 4 => 2*(3/(1+mu))^2 = 4

# => (1+mu)^2 = 9/2 => 1+mu = 3/sqrt(2) => mu = 3/sqrt(2) - 1

mu = 3/np.sqrt(2) - 1

x_opt = 3 / (1 + mu)

y_opt = 3 / (1 + mu)

print(f'mu = {mu:.4f} (>0: dual feasibility satisfied)')

print(f'x = y = {x_opt:.4f}')

print(f'Constraint: x^2+y^2 = {x_opt**2 + y_opt**2:.4f} (active at boundary)')

fig, ax = plt.subplots(figsize=(6, 6))

X2, Y2 = np.meshgrid(np.linspace(-3, 4, 300), np.linspace(-3, 4, 300))

F2 = (X2-3)**2 + (Y2-3)**2

ax.contourf(X2, Y2, F2, levels=20, cmap='YlOrRd_r', alpha=0.7)

ax.contour(X2, Y2, F2, levels=20, colors='orange', linewidths=0.5, alpha=0.6)

theta = np.linspace(0, 2*np.pi, 300)

ax.fill(2*np.cos(theta), 2*np.sin(theta), alpha=0.2, color='green', label='feasible region')

ax.plot(2*np.cos(theta), 2*np.sin(theta), 'g-', lw=2)

ax.plot(3, 3, 'bx', ms=12, mew=3, label='unconstrained min (3,3)')

ax.plot(x_opt, y_opt, 'ko', ms=10, zorder=5, label=f'constrained min ({x_opt:.2f},{y_opt:.2f})')

ax.plot([x_opt, 3], [y_opt, 3], 'k--', alpha=0.5)

ax.set_xlabel('x'); ax.set_ylabel('y')

ax.set_title('KKT: Inequality Constraint (active boundary)')

ax.legend(loc='upper left'); ax.set_aspect('equal')

plt.tight_layout()

plt.savefig('ch233_kkt.png', dpi=120)

plt.show()mu = 1.1213 (>0: dual feasibility satisfied)

x = y = 1.4142

Constraint: x^2+y^2 = 4.0000 (active at boundary)

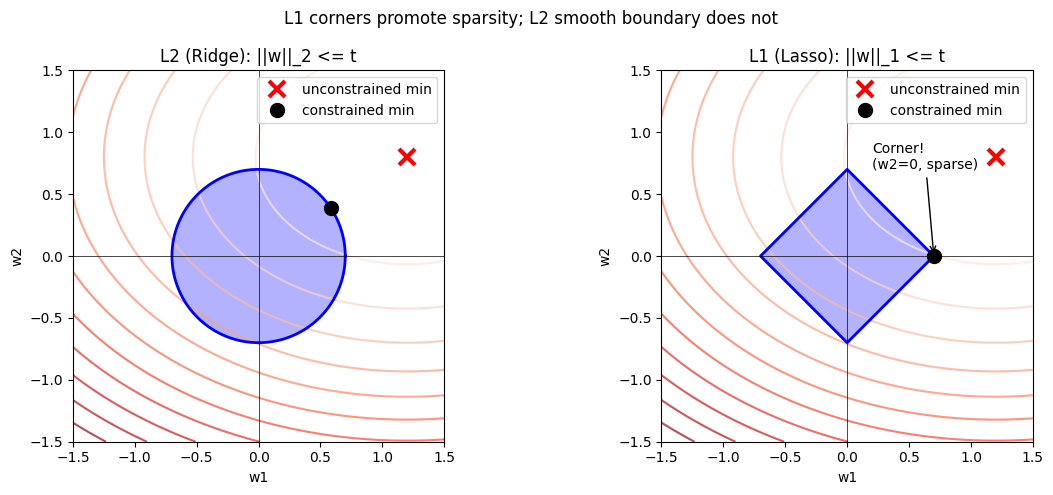

3. L2 Regularisation as a Constrained Problem¶

Ridge regression is normally written as: minimise ||y - Xw||² + λ||w||²

This is equivalent to: minimise ||y - Xw||² subject to ||w||² ≤ t(λ)

The regularisation parameter λ is the Lagrange multiplier. Larger λ = tighter constraint = smaller weights. L1 regularisation (Lasso) uses ||w||₁ ≤ t, whose constraint boundary has corners — this is why Lasso produces sparse solutions.

# Visualise L1 vs L2 constraint regions and why L1 promotes sparsity

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

for ax, norm, title in zip(axes, [2, 1], ['L2 (Ridge): ||w||_2 <= t', 'L1 (Lasso): ||w||_1 <= t']):

w1 = np.linspace(-1.5, 1.5, 400)

w2 = np.linspace(-1.5, 1.5, 400)

W1, W2 = np.meshgrid(w1, w2)

# Loss landscape (shifted from origin to create interesting intersection)

w1_star, w2_star = 1.2, 0.8

Loss = (W1 - w1_star)**2 + 2*(W2 - w2_star)**2

ax.contour(W1, W2, Loss, levels=15, cmap='Reds', alpha=0.7)

# Constraint region

t = 0.7

if norm == 2:

theta = np.linspace(0, 2*np.pi, 300)

cx, cy = t*np.cos(theta), t*np.sin(theta)

ax.fill(cx, cy, alpha=0.3, color='blue')

ax.plot(cx, cy, 'b-', lw=2)

# Minimum is on the circle, not at a corner

# Approximate: project (w1_star, w2_star) onto circle

angle = np.arctan2(w2_star, w1_star)

w_constrained = np.array([t*np.cos(angle), t*np.sin(angle)])

else:

# L1 ball is a diamond

corners = np.array([[t,0],[0,t],[-t,0],[0,-t],[t,0]])

ax.fill(corners[:,0], corners[:,1], alpha=0.3, color='blue')

ax.plot(corners[:,0], corners[:,1], 'b-', lw=2)

# Minimum often hits a corner (sparse solution)

w_constrained = np.array([t, 0.0])

ax.plot(w1_star, w2_star, 'rx', ms=12, mew=3, label='unconstrained min')

ax.plot(w_constrained[0], w_constrained[1], 'ko', ms=10, label='constrained min')

ax.axhline(0, color='k', lw=0.5); ax.axvline(0, color='k', lw=0.5)

ax.set_xlabel('w1'); ax.set_ylabel('w2')

ax.set_title(title); ax.legend(); ax.set_aspect('equal')

ax.set_xlim(-1.5, 1.5); ax.set_ylim(-1.5, 1.5)

axes[1].annotate('Corner!\n(w2=0, sparse)', xy=(t, 0), xytext=(0.2, 0.7),

arrowprops=dict(arrowstyle='->', color='black'), fontsize=10)

plt.suptitle('L1 corners promote sparsity; L2 smooth boundary does not', fontsize=12)

plt.tight_layout()

plt.savefig('ch233_regularisation.png', dpi=120)

plt.show()

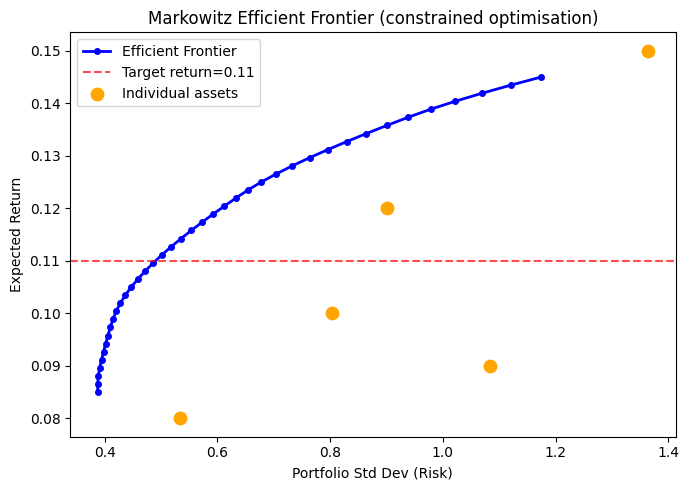

4. Numerical Constrained Optimisation with scipy¶

from scipy.optimize import minimize

# Portfolio optimisation: minimise variance, target return >= r_min

# weights w, returns mu, covariance Sigma

np.random.seed(42)

n_assets = 5

mu_assets = np.array([0.10, 0.12, 0.08, 0.15, 0.09]) # expected returns

# Random positive-definite covariance

A = np.random.randn(n_assets, n_assets)

Sigma = A.T @ A / n_assets + 0.05 * np.eye(n_assets)

def portfolio_variance(w):

return w @ Sigma @ w

def portfolio_return(w):

return mu_assets @ w

r_min = 0.11 # target return

constraints = [

{'type': 'eq', 'fun': lambda w: np.sum(w) - 1}, # weights sum to 1

{'type': 'ineq', 'fun': lambda w: portfolio_return(w) - r_min} # return >= r_min

]

bounds = [(0, 1)] * n_assets # no short selling

w0 = np.ones(n_assets) / n_assets

result = minimize(portfolio_variance, w0, method='SLSQP',

bounds=bounds, constraints=constraints)

print('Optimisation result:', result.message)

print(f'Weights: {result.x.round(4)}')

print(f'Portfolio variance: {result.fun:.6f}')

print(f'Portfolio return: {portfolio_return(result.x):.4f} (target >= {r_min})')

print(f'Weights sum: {result.x.sum():.6f}')Optimisation result: Optimization terminated successfully

Weights: [0.289 0.2533 0.2564 0.2013 0. ]

Portfolio variance: 0.240347

Portfolio return: 0.1100 (target >= 0.11)

Weights sum: 1.000000

# Efficient frontier: trace the minimum variance for each target return

returns_range = np.linspace(0.085, 0.145, 40)

variances = []

for r_target in returns_range:

cons = [

{'type': 'eq', 'fun': lambda w: np.sum(w) - 1},

{'type': 'ineq', 'fun': lambda w, r=r_target: portfolio_return(w) - r}

]

res = minimize(portfolio_variance, w0, method='SLSQP',

bounds=bounds, constraints=cons)

variances.append(res.fun if res.success else np.nan)

fig, ax = plt.subplots(figsize=(7, 5))

ax.plot(np.sqrt(variances), returns_range, 'b-o', ms=4, lw=2, label='Efficient Frontier')

ax.axhline(r_min, color='red', linestyle='--', alpha=0.7, label=f'Target return={r_min}')

ax.scatter(np.sqrt(np.diag(Sigma)), mu_assets, c='orange', s=80, zorder=5, label='Individual assets')

ax.set_xlabel('Portfolio Std Dev (Risk)')

ax.set_ylabel('Expected Return')

ax.set_title('Markowitz Efficient Frontier (constrained optimisation)')

ax.legend()

plt.tight_layout()

plt.savefig('ch233_frontier.png', dpi=120)

plt.show()

5. Summary¶

| Concept | Key Idea |

|---|---|

| Lagrange multipliers | At constrained minimum, ∇f ∥ ∇g |

| KKT conditions | Extend Lagrange to inequality constraints |

| Complementary slackness | μ·g(x)=0: either constraint active or multiplier zero |

| L2 regularisation | Equivalent to weight-norm equality constraint |

| L1 regularisation | Diamond constraint; corners produce sparsity |

| scipy SLSQP | Sequential Least SQuares Programming solver |

6. Forward References¶

The KKT complementary slackness condition reappears in ch291 — Optimisation Methods, where we derive support vector machines formally.

The efficient frontier construction previews ch271 — Data and Measurement and ch293 — Clustering, where risk-return tradeoffs model real portfolio decisions.

L1 sparsity connects to ch298 — Information Theory: sparse representations minimise redundancy.