Part VIII: Probability¶

Simulation is the empirical arm of probability. When a system is too complex for closed-form analysis, you simulate it — generate realizations of the random process, observe outcomes, and estimate quantities of interest. This chapter assembles the core toolkit: inverse transform sampling, rejection sampling, the Gillespie algorithm for continuous-time processes, and Euler-Maruyama for stochastic differential equations.

Prerequisites: Probability Distributions (ch248), Random Variables (ch247), Random Walks (ch258), Monte Carlo Methods (ch256), Numerical Integration (ch221).

1. Inverse Transform Sampling¶

If is a CDF and , then has distribution . This is exact and works for any distribution with an invertible CDF (CDF introduced in ch248).

Proof: .

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

rng = np.random.default_rng(42)

# Sample from Exponential(lambda=2) via inverse transform

# CDF: F(x) = 1 - e^(-lambda x) => F^{-1}(u) = -log(1-u)/lambda

def sample_exponential_via_it(lam, n, rng):

"""Sample Exponential(lambda) via inverse transform."""

u = rng.uniform(0, 1, n)

return -np.log(1 - u) / lam # F^{-1}(u)

# Sample from a custom discrete distribution via inverse transform

def sample_discrete_via_it(values, probs, n, rng):

"""Sample from a discrete distribution using inverse CDF.

Args:

values: array of possible values

probs: array of probabilities (must sum to 1)

n: number of samples

rng: numpy random generator

Returns:

samples from the specified discrete distribution

"""

cdf = np.cumsum(probs)

u = rng.uniform(0, 1, n)

indices = np.searchsorted(cdf, u)

return values[np.clip(indices, 0, len(values)-1)]

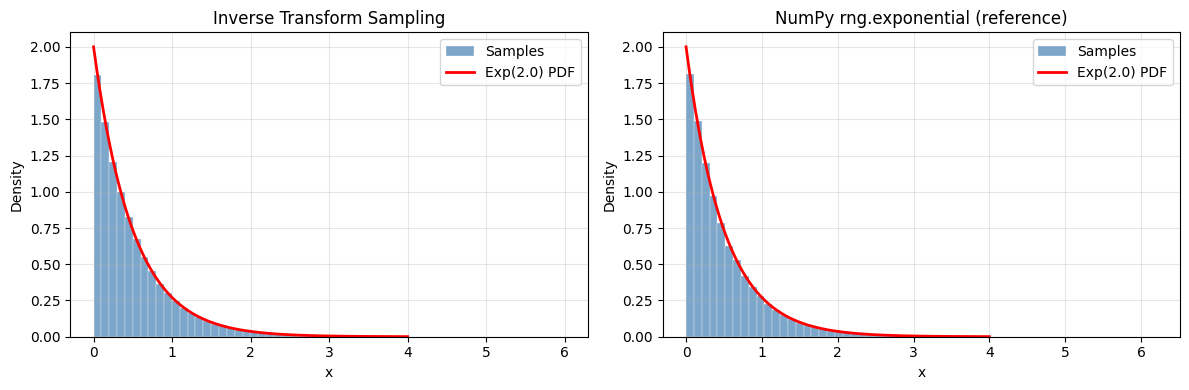

lam = 2.0

N = 100_000

samples_it = sample_exponential_via_it(lam, N, rng)

samples_scipy = rng.exponential(1/lam, N) # scipy uses scale = 1/lambda

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

x_range = np.linspace(0, 4, 300)

true_pdf = stats.expon.pdf(x_range, scale=1/lam)

for ax, samples, title in zip(axes,

[samples_it, samples_scipy],

['Inverse Transform Sampling', 'NumPy rng.exponential (reference)']):

ax.hist(samples, bins=60, density=True, alpha=0.7, color='steelblue',

edgecolor='white', linewidth=0.3, label='Samples')

ax.plot(x_range, true_pdf, 'r-', linewidth=2, label=f'Exp({lam}) PDF')

ax.set_title(title)

ax.set_xlabel('x')

ax.set_ylabel('Density')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('inverse_transform.png', dpi=120, bbox_inches='tight')

plt.show()

ks_stat, ks_p = stats.kstest(samples_it, 'expon', args=(0, 1/lam))

print(f"KS test: statistic={ks_stat:.4f}, p-value={ks_p:.4f} (p >> 0.05 = good)")

KS test: statistic=0.0030, p-value=0.3313 (p >> 0.05 = good)

2. Rejection Sampling¶

When is unavailable, rejection sampling samples from a proposal (where is a constant, ) and accepts with probability .

Acceptance rate = . Choose the tightest proposal possible.

def rejection_sample(target_pdf, proposal_sampler, proposal_pdf, M, n_samples, rng):

"""Rejection sampling: sample from target_pdf using proposal.

Args:

target_pdf: callable, unnormalized target density p(x)

proposal_sampler: callable(n) -> samples from proposal q

proposal_pdf: callable, proposal density q(x)

M: bounding constant such that p(x) <= M * q(x) for all x

n_samples: desired number of accepted samples

rng: numpy random generator

Returns:

accepted: array of accepted samples

acceptance_rate: fraction of proposals accepted

"""

accepted = []

total_proposed = 0

batch_size = max(n_samples * 2, 1000) # over-sample in batches

while len(accepted) < n_samples:

x = proposal_sampler(batch_size)

u = rng.uniform(0, 1, batch_size)

accept_prob = target_pdf(x) / (M * proposal_pdf(x))

mask = u < accept_prob

accepted.extend(x[mask].tolist())

total_proposed += batch_size

accepted = np.array(accepted[:n_samples])

return accepted, len(accepted) / total_proposed

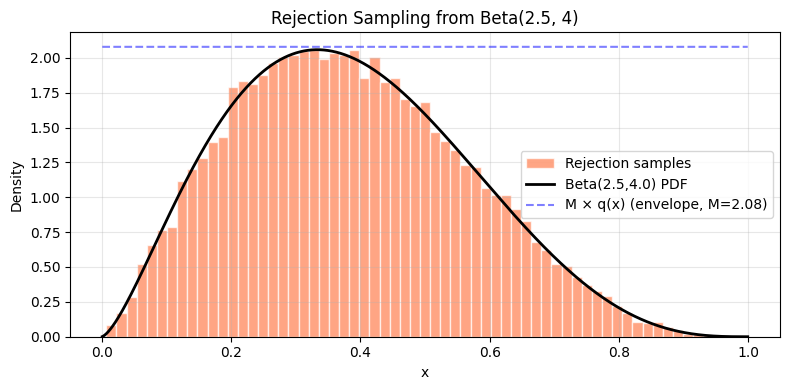

# Target: Beta(2.5, 4) — no simple inverse CDF

# Proposal: Uniform(0,1)

alpha_b, beta_b = 2.5, 4.0

def beta_pdf(x):

return stats.beta.pdf(x, alpha_b, beta_b)

# M = max of beta PDF (numerical)

x_grid = np.linspace(0.001, 0.999, 10000)

M = beta_pdf(x_grid).max() * 1.01 # slight buffer

samples_rs, accept_rate = rejection_sample(

target_pdf=beta_pdf,

proposal_sampler=lambda n: rng.uniform(0, 1, n),

proposal_pdf=lambda x: np.ones_like(x), # Uniform(0,1) density = 1

M=M,

n_samples=20_000,

rng=rng

)

print(f"Beta({alpha_b}, {beta_b}) via rejection sampling:")

print(f" Acceptance rate: {accept_rate:.3f} (theoretical 1/M = {1/M:.3f})")

print(f" Sample mean: {samples_rs.mean():.4f} (true: {alpha_b/(alpha_b+beta_b):.4f})")

fig, ax = plt.subplots(figsize=(8, 4))

ax.hist(samples_rs, bins=60, density=True, alpha=0.7, color='coral',

edgecolor='white', label='Rejection samples')

ax.plot(x_grid, beta_pdf(x_grid), 'k-', linewidth=2, label=f'Beta({alpha_b},{beta_b}) PDF')

ax.plot(x_grid, M * np.ones_like(x_grid), 'b--', linewidth=1.5,

alpha=0.5, label=f'M × q(x) (envelope, M={M:.2f})')

ax.set_xlabel('x')

ax.set_ylabel('Density')

ax.set_title('Rejection Sampling from Beta(2.5, 4)')

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('rejection_sampling.png', dpi=120, bbox_inches='tight')

plt.show()Beta(2.5, 4.0) via rejection sampling:

Acceptance rate: 0.250 (theoretical 1/M = 0.481)

Sample mean: 0.3856 (true: 0.3846)

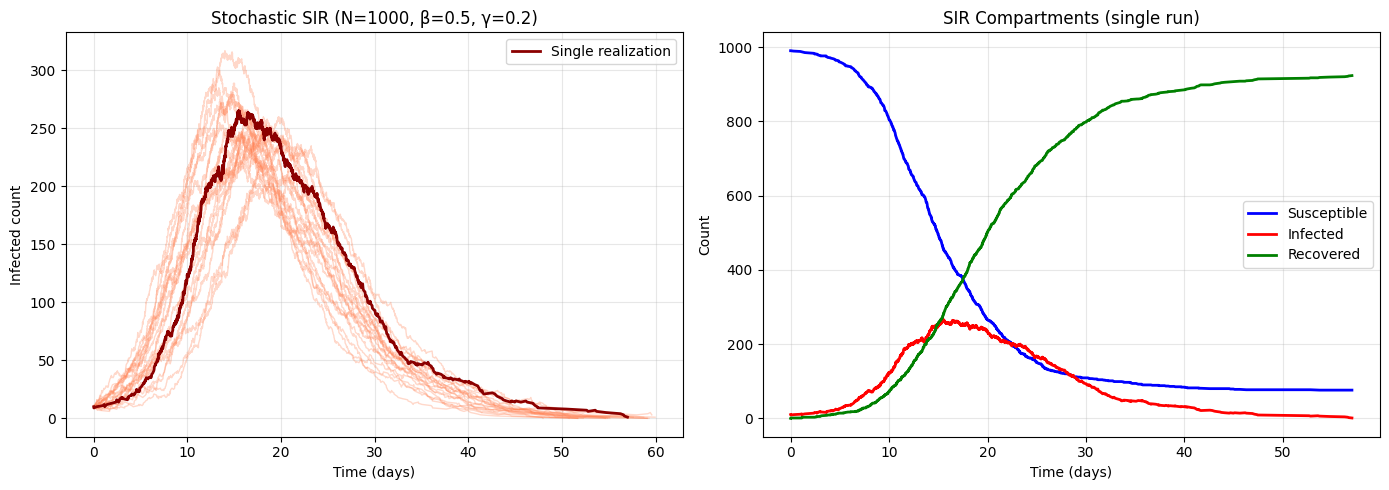

3. Simulating Continuous-Time Processes: Gillespie Algorithm¶

Discrete event systems (chemical reactions, birth-death processes, queueing) evolve in continuous time with random event times. The Gillespie algorithm (exact stochastic simulation):

Compute total rate (sum of all event rates)

Sample next event time:

Sample which event occurs: proportional to

Update state; repeat

def gillespie_sir(S0, I0, R0, beta, gamma, t_max, rng):

"""Exact stochastic SIR epidemic model via Gillespie algorithm.

Events:

Infection: S -> I at rate beta*S*I/N

Recovery: I -> R at rate gamma*I

Args:

S0, I0, R0: initial counts

beta: infection rate

gamma: recovery rate

t_max: maximum simulation time

rng: numpy random generator

Returns:

times, S_traj, I_traj, R_traj: arrays of states at event times

"""

N = S0 + I0 + R0

S, I, R = S0, I0, R0

t = 0.0

times = [t]

S_traj, I_traj, R_traj = [S], [I], [R]

while t < t_max and I > 0:

# Event rates

rate_infect = beta * S * I / N

rate_recover = gamma * I

total_rate = rate_infect + rate_recover

if total_rate == 0:

break

# Time to next event

dt = rng.exponential(1.0 / total_rate)

t += dt

if t > t_max:

break

# Which event?

if rng.random() < rate_infect / total_rate:

S -= 1

I += 1

else:

I -= 1

R += 1

times.append(t)

S_traj.append(S)

I_traj.append(I)

R_traj.append(R)

return np.array(times), np.array(S_traj), np.array(I_traj), np.array(R_traj)

# Parameters: R0 = beta/gamma = 2.5

S0, I0, R0 = 990, 10, 0

beta, gamma = 0.5, 0.2

t_max = 60

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Multiple stochastic realizations

n_sims = 20

peak_infecteds = []

for trial in range(n_sims):

times, S_t, I_t, R_t = gillespie_sir(S0, I0, R0, beta, gamma, t_max, rng)

axes[0].plot(times, I_t, alpha=0.3, linewidth=1, color='coral')

peak_infecteds.append(I_t.max())

# One highlighted trajectory

times, S_t, I_t, R_t = gillespie_sir(S0, I0, R0, beta, gamma, t_max, rng)

axes[0].plot(times, I_t, 'darkred', linewidth=2, label='Single realization')

axes[0].set_xlabel('Time (days)')

axes[0].set_ylabel('Infected count')

axes[0].set_title(f'Stochastic SIR (N={S0+I0+R0}, β={beta}, γ={gamma})')

axes[0].legend()

axes[0].grid(True, alpha=0.3)

# Full compartment view

axes[1].plot(times, S_t, 'b-', linewidth=2, label='Susceptible')

axes[1].plot(times, I_t, 'r-', linewidth=2, label='Infected')

axes[1].plot(times, R_t, 'g-', linewidth=2, label='Recovered')

axes[1].set_xlabel('Time (days)')

axes[1].set_ylabel('Count')

axes[1].set_title('SIR Compartments (single run)')

axes[1].legend()

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('gillespie_sir.png', dpi=120, bbox_inches='tight')

plt.show()

print(f"Peak infected across {n_sims} simulations:")

print(f" Mean: {np.mean(peak_infecteds):.1f}")

print(f" Std: {np.std(peak_infecteds):.1f}")

print(f" Min: {np.min(peak_infecteds)}")

print(f" Max: {np.max(peak_infecteds)}")

Peak infected across 20 simulations:

Mean: 258.3

Std: 25.1

Min: 210

Max: 317

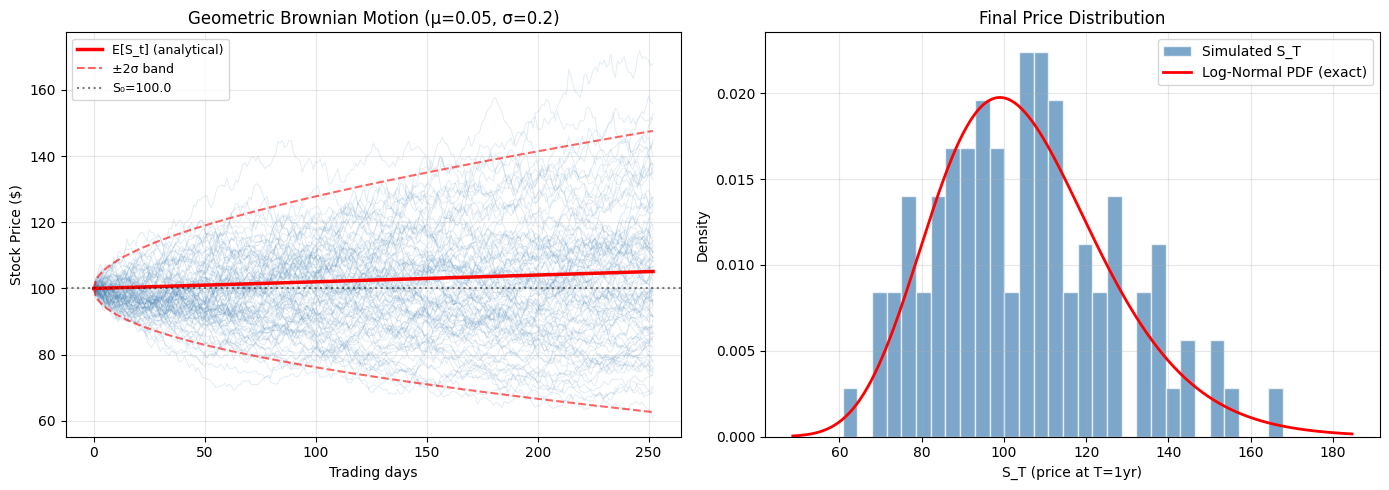

4. Euler-Maruyama: Simulating Stochastic Differential Equations¶

A stochastic differential equation (SDE) is:

where , (Brownian increment). The Euler-Maruyama discretization:

Application: Geometric Brownian Motion (GBM) models stock prices: →

def euler_maruyama(mu_fn, sigma_fn, x0, T, n_steps, n_paths, rng):

"""Euler-Maruyama simulation of an SDE.

Args:

mu_fn: drift function (x, t) -> scalar

sigma_fn: diffusion function (x, t) -> scalar

x0: initial value

T: final time

n_steps: number of time steps

n_paths: number of independent paths

rng: numpy random generator

Returns:

t_grid: time grid (n_steps+1,)

paths: (n_steps+1, n_paths) array of simulated paths

"""

dt = T / n_steps

t_grid = np.linspace(0, T, n_steps + 1)

paths = np.zeros((n_steps + 1, n_paths))

paths[0] = x0

sqrt_dt = np.sqrt(dt)

for i in range(n_steps):

t = t_grid[i]

x = paths[i]

Z = rng.standard_normal(n_paths)

drift = np.vectorize(mu_fn)(x, t)

diffusion = np.vectorize(sigma_fn)(x, t)

paths[i+1] = x + drift * dt + diffusion * sqrt_dt * Z

return t_grid, paths

# Geometric Brownian Motion: dS = mu*S dt + sigma*S dW

S0 = 100.0

mu_gbm = 0.05 # 5% annual drift

sigma_gbm = 0.20 # 20% annual volatility

T = 1.0 # 1 year

n_steps = 252 # daily steps

n_paths = 100

t_grid, paths = euler_maruyama(

mu_fn=lambda x, t: mu_gbm * x,

sigma_fn=lambda x, t: sigma_gbm * x,

x0=S0, T=T, n_steps=n_steps, n_paths=n_paths,

rng=rng

)

# Analytical solution

t_fine = np.linspace(0, T, 300)

analytical_mean = S0 * np.exp(mu_gbm * t_fine)

analytical_std = S0 * np.exp(mu_gbm * t_fine) * np.sqrt(np.exp(sigma_gbm**2 * t_fine) - 1)

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

for i in range(n_paths):

axes[0].plot(t_grid * 252, paths[:, i], alpha=0.15, linewidth=0.7, color='steelblue')

axes[0].plot(t_fine * 252, analytical_mean, 'r-', linewidth=2.5, label='E[S_t] (analytical)')

axes[0].plot(t_fine * 252, analytical_mean + 2*analytical_std, 'r--', linewidth=1.5,

alpha=0.6, label='±2σ band')

axes[0].plot(t_fine * 252, analytical_mean - 2*analytical_std, 'r--', linewidth=1.5, alpha=0.6)

axes[0].axhline(S0, color='black', linestyle=':', alpha=0.5, label=f'S₀={S0}')

axes[0].set_xlabel('Trading days')

axes[0].set_ylabel('Stock Price ($)')

axes[0].set_title(f'Geometric Brownian Motion (μ={mu_gbm}, σ={sigma_gbm})')

axes[0].legend(fontsize=9)

axes[0].grid(True, alpha=0.3)

# Final distribution

final_prices = paths[-1]

axes[1].hist(final_prices, bins=30, density=True, color='steelblue',

alpha=0.7, edgecolor='white', label='Simulated S_T')

# Log-normal analytical distribution

log_mean = np.log(S0) + (mu_gbm - 0.5*sigma_gbm**2) * T

log_std = sigma_gbm * np.sqrt(T)

x_range = np.linspace(final_prices.min()*0.8, final_prices.max()*1.1, 300)

axes[1].plot(x_range, stats.lognorm.pdf(x_range, s=log_std, scale=np.exp(log_mean)),

'r-', linewidth=2, label='Log-Normal PDF (exact)')

axes[1].set_xlabel('S_T (price at T=1yr)')

axes[1].set_ylabel('Density')

axes[1].set_title('Final Price Distribution')

axes[1].legend()

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('gbm_simulation.png', dpi=120, bbox_inches='tight')

plt.show()

print(f"Final price statistics (N={n_paths} paths):")

print(f" Simulated mean: ${final_prices.mean():.2f} (theoretical: ${S0*np.exp(mu_gbm*T):.2f})")

print(f" Simulated std: ${final_prices.std():.2f} (theoretical: ${analytical_std[-1]:.2f})")

Final price statistics (N=100 paths):

Simulated mean: $105.12 (theoretical: $105.13)

Simulated std: $21.79 (theoretical: $21.24)

5. Summary¶

| Technique | When to use | Complexity |

|---|---|---|

| Inverse Transform | CDF invertible analytically | O(n) |

| Rejection Sampling | Target density known up to constant | O(n/acceptance_rate) |

| Gillespie | Exact continuous-time discrete events | O(n_events) |

| Euler-Maruyama | SDEs, approximate continuous paths | O(n_paths × n_steps) |

9. Forward References¶

ch260 — Project: Monte Carlo π: Applies basic simulation (geometric sampling) in a complete project.

ch283 — Bayesian Statistics (Part IX): Markov Chain Monte Carlo (MCMC) combines ch257 and this chapter — a Markov chain whose stationary distribution is the posterior, sampled via Metropolis-Hastings (a form of rejection sampling with memory).

ch298 — Build a Mini ML Library (Part IX): Stochastic gradient descent uses random sampling (mini-batches) as a computational simulation technique — the same randomness-for-tractability philosophy.